New, over-strict norms are killing e-commerce

05 Mar 2011

Two things are a dampener to e-commerce market in India. One is the introduction of something called two factor authentications for credit card transactions on the net, and over secure IVR (inter-active voice response); and the second is Mobile Money ID (MMID) for instant mobile fund transfer. The former throttles e-commerce, and the latter mobile commerce.

Take the first issue. There are 13 million internet users who actively engage in web-based transactions. People are just getting comfortable with e-commerce for railway or airline tickets, e-shopping, holidays, financial services, classified advertising, etc.

Take the first issue. There are 13 million internet users who actively engage in web-based transactions. People are just getting comfortable with e-commerce for railway or airline tickets, e-shopping, holidays, financial services, classified advertising, etc.

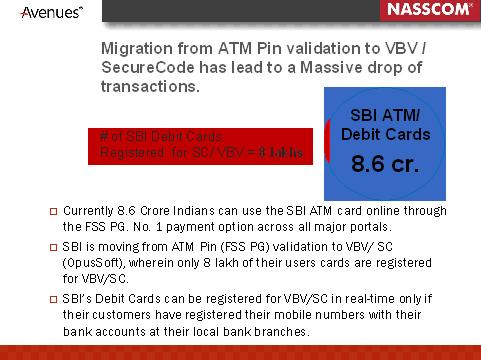

But that was till 2 FA came into being, viz Verified by Visa (VBV) and Secure Code. Now as a result, just 1 per cent of the State Bank of India's debit card base stands registered for VBV. It is not known how many of this one per cent are active today. But travel portal Cleartrip has seen a 73-per cent drop in transactions! Clearly not only is merchant traffic drastically low, but consumers are confused with different practices by different banks and card companies.

Thus far, the cleanest implementation is by Amex. It has a simple address verification system (AVS) for its e-commerce, and postal code of its customer as its one time password (OTP) for IVR transactions. So the solution for IVR transactions is 'OTFP' or 'one time fixed password' such as postal code, date of birth or credit/debit card PIN No.

(Source: Nasscom)

If we don't move to this simple method for ensuring the same level of security we will be presiding over a shrinking e-commerce market, not one supposed to expand by 50 per cent this year! In fact there is no evidence of any fraud or charge-back arising from mobile, whether it is use of an app or sms or IVR. In fact it is less than any other accredited retail financial instruments in play today.

On MMID, this was introduced for enabling inter-bank account to account transfer using mobile (called IMPS), under the umbrella of the National Payments Corporation of India. Here again usage of this is dismal. Over a million MMID's may have been issued, but only less than a thousand have transacted. Of a banking population of over 400 million!

The user experience is clumsy, and involves many hoops to jump through. I have suggested some work around to NPCI in trying to simplify the whole experience with minimum key strokes, interlinks, and without taxing an average person's memory.

Here NPCI becomes a repository for all registered IMPS users, and the consumer need only use a MPIN number for authentication. The transaction (routing) goes through without the sender or beneficiary having to remember each others accounts and MMIDs. In addition, the use of SMS or IVR to fulfill a fund transfer is a further boost to making it available and user friendly to the lowest common denominator of phone type and data plan. The true aam admi utility.