Demand for office space in India rises in Q1 2011

13 Apr 2011

The first quarter of 2011 saw almost six million sq ft of office space being absorbed across key markets in India, representing a 20 per cent increase over Q1 of 2010, according to CB Richard Ellis, an international real estate consultancy.

India's IT hub Bangalore accounted for 36 per cent (more than two million sq ft) of total office space absorbed in Q1 of the year, followed by the National Capital Region (NCR) at 27 per cent. In 2010, a total of 32 million sq ft of office space was absorbed in India, says the report – India office market view – Q1, 2011 – by CB Richard Ellis.

India's IT hub Bangalore accounted for 36 per cent (more than two million sq ft) of total office space absorbed in Q1 of the year, followed by the National Capital Region (NCR) at 27 per cent. In 2010, a total of 32 million sq ft of office space was absorbed in India, says the report – India office market view – Q1, 2011 – by CB Richard Ellis.

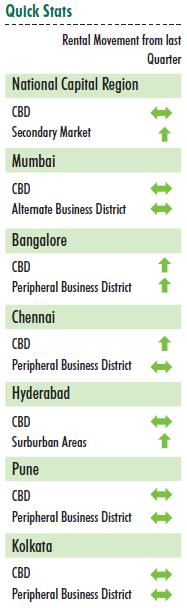

The report reviews rentals for grade A office space in Delhi NCR, Mumbai, Bangalore, Chennai, Hyderabad, Pune and Kolkata.

''The office market across India continues to grow as is evident from the findings of our report,'' says Anshuman Magazine, managing director, CB Richard Ellis. ''With corporates renewing their expansion plans across most industry sectors, both demand levels and transaction velocity are expected to remain buoyant in the near to mid-term.

However with the significant supply in the market, rentals are expected to remain under pressure except for Grade A office space in few key micro markets.''

The rental values for grade A office space largely remained stable across most non-CBD and suburban micro-markets, says the report. Whilst demand levels have been positive, the large supply pipeline and ready availability of quality space has negated any undue price enhancement.

In some micro markets, high vacancy levels could contribute to development of some downward pressure on values in the short to medium term. Values in the central business district (CBD) locations in Delhi, Pune, Kolkata and Hyderabad remained stable, whilst those in Bangalore and Chennai witnessed enhancement.

The first quarter of 2011 witnessed the addition of a total of 7.07 million sq ft of new supply across NCR, Mumbai and Bangalore, contributing more than 60 pe cent of the total supply which came on stream.

Rental market indicators

| Sub-market | Average Rent in March 11 (INR per sq ft per month) | Average Rent in Dec 10 (INR per sq ft per month) |

| CBD (Connaught Place) Grade A | 250 | 250 |

| CBD (Connaught Place) Grade B | 145 | 145 |

| Secondary market (Nehru Place) Grade A | 170 | 150 |

| Secondary market (Jasola) Grade A | 115 | 115 |

| Secondary market ( Saket) Grade A | 133 | 133 |

| Gurgaon Grade A Commercial | 75 | 70 |

| Gurgaon Grade A IT | 50 | 48 |

| NOIDA Grade A IT | 30 | 30 |

In Mumbai, Nariman Point witnessed limited activity with negligible supply addition, and absorption was recorded at around 10,000 sq ft. Rental values remained stable, while capital values increased by 20 per cent, says the research report. About 350,000 sq ft of IT space became available in the extended business district (EBD) of Lower Parel during the first quarter of 2011.

The Bandra Kurla Complex (BKC) also witnessed limited transaction activity with no fresh supply added during this quarter. The BKC has emerged as a new CBD in Mumbai, rivalling Nariman Point.

Rental market indicators

| Sub-market | Average Rent in Mar 10 (INR per sq ft per month) | Average Rent in Dec 10 (INR per sq ft per month) |

| CBD (Nariman Point, Fort, Cuffe Parade) Grade A | 300 | 300 |

| CBD (Nariman Point, Fort, Cuffe Parade) Grade B | 250 | 200 |

| EBD ( Lower Parel) Grade A | 155 | 160 |

| EBD (Worli, Prabhadevi) Grade A | 270 | 265 |

| ABD (Bandra Kurla Complex, Kalina) Grade A | 285 | 285 |

| ABD (Bandra Kurla Complex, Kalina) Grade B | 240 | 190 |

| SBD (Andheri, Vile Parle, Jogeshwari) Grade A | 120 | 120 |

| SBD (Andheri, Vile Parle, Jogeshwari) Grade B | 90 | 85 |

| PBD (Malad) Grade A | 65 | 65 |

| PBD (Powai,Vikhroli) Grade A | 85 | 85 |

| PBD (Thane, New Mumbai) Grade A | 45 | 45 |

CB Richard Ellis Group, Inc. is a Fortune 500 and S&P 500 company headquartered in Los Angeles, and is the world's largest commercial real estate services firm. It was the first independent international real estate consultancy to have a presence in India with an office in New Delhi in 1994.

Rental market indicators

| Sub-market | Average Rent in Mar 11 (INR per sq ft per month) | Average Rent in Dec 10 (INR per sq ft per month) |

| CBD (MG Road, Residency Road) Grade A | 85 | 74 |

| CBD (MG Road, Residency Road) Grade B | 69 | 60 |

| EBD (Koramagala, Indiranagar) Grade A | 60 | 55 |

| EBD (Karamangala, Indiranagar) Grade B | 48 | 42 |

| Outer Ring Road Grade A | 44 | 42 |

| Outer Ring Road Grade B | 42 | 36 |

| Whitefield, Electronic City Grade A | 30 | 24 |